Deal Structuring

Make Lenders Fall in Love with Your Deal: 5 Moves That Close

By Drew Eckman · BayCoastJune 17, 202612 min read

If you're a self-funded searcher who gets a business under LOI, congratulations are in order. It's easy for folks in the ETA ecosystem, whether it's prospective investors, existing owners, or other advisors, to downplay this with a "now the real work begins!"

Fair enough. But in today's market it's harder than ever to get a strong deal under LOI. So I'll be the one to say congratulations, because it's worth taking a moment to celebrate. And after that celebratory moment, and a deep breath, you should then ask: "How do I position this deal most favorably to lenders and investors?"

That's where we come in. At BayCoast, we've worked with hundreds of acquisition entrepreneurs as they start a search, secure a deal, and then figure out how to position that deal in the most favorable light. This article focuses on lenders, who think very differently than investors. Below are five ways to make lenders fall in love with your deal.

Tip #1: Underwrite Cash Flow Like a Lender

The best buyers can not only describe what happened in a company's financials, but why it happened. In other words, they understand the story behind the numbers.

As a buyer, it's easy to get caught up in the multiple of earnings you are paying. You might frame a deal as "TTM EBITDA is $X, and I have the deal under LOI for 3.9x." Sounds great.

But too often we see buyers who haven't really examined the last three years' results and can't thoughtfully explain what's driving revenue growth, gross margin expansion (or compression), and, ultimately, cash flow.

Consider a hypothetical. A buyer finds a business right in the sweet spot for a self-funded searcher: $750K EBITDA at a 4.0x multiple ($3.0M purchase price). Further assume a popular 80/10/10 structure: 80% SBA debt, 10% seller note, and 10% equity. The final sources and uses of funds might look something like this:

| Sources | $ | % of Total | Uses | $ | % of Total |

|---|---|---|---|---|---|

| Senior Debt | 2,550,000 | 79.7% | Purchase Price | 3,000,000 | 93.8% |

| Seller Note(s) | 300,000 | 9.4% | Excess Cash to BS | 50,000 | 1.6% |

| Buyer Equity | 350,000 | 10.9% | SBA Gty Fee | 69,219 | 2.2% |

| Trans. Expenses | 80,781 | 2.5% | |||

| Total Sources | 3,200,000 | 100.0% | Total Uses | 3,200,000 | 100.0% |

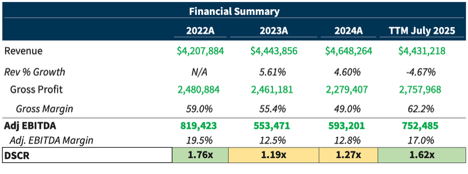

We made some assumptions on the seller note terms, but assume for our illustration that annual debt service is $465,000. The debt service coverage ratio (DSCR) appears healthy. $750K divided by $465K = 1.6. But now consider the last three years' results.

This should raise some questions for our buyer. Should you expect gross margin to be 50%? Or closer to 60%? Why did margins weaken in 2023 and 2024, only to rebound in the TTM period? What's "normal" for the industry? How does what's normal compare to our target? How did EBITDA margin improve in 2024 despite gross margin falling to 49%?

The best buyers aren't afraid to be the "dumbest" person in the room with the seller and ask what's driving the results. Sometimes there are good answers. Other times, the seller doesn't quite know. In either case, the numbers must back up the seller's story. Why are you confident the same issues won't happen to you when you take over?

One of the most common mistakes I see first-time buyers make is failing to look at the last three years' results, especially DSCR by year. That's a sure-fire way to put your deal in jeopardy.

Finally, you must tie your analysis to the tax returns. Build from net income to adjusted EBITDA (the numerator that lenders will use in calculating DSCR):

- Collect the last 3 years of tax returns.

- Start with net income.

- Add back interest, tax, depreciation, and amortization (per the tax return) to get book EBITDA.

- Add back sensible, provable addbacks (such as the owner's compensation).

- Subtract pro-forma expenses (like the salary you are going to pay yourself).

The headline multiple isn't what determines whether your deal works. A three-year, tax-return based view of EBITDA and DSCR tells you what valuation and structure actually work.

If you want help with pre-LOI structuring (including levers like seller note terms or a two-note structure) to improve DSCR, we offer complimentary pre-LOI consultations at BayCoast. Book a call with us or email me at drew@baycoastadvisors.com.

Tip #2: Include Sensible, Provable Addbacks Only

If you've looked at brokered deals, you've undoubtedly seen a wide range of claimed "addbacks." What makes SBA financing difficult is deciding whether a lender will accept those addbacks.

Here's a question we get all the time at BayCoast: can you tell me exactly what addbacks lenders will accept? Rather than give you a list that categorically declares which addbacks are a "yes" and a "no," it's far more helpful for you to have a framework for evaluating addbacks. Here's the framework we find most useful:

- Is this expense one-time or recurring?

- Will you have this expense or a related expense post-closing?

- Can it be documented and proven?

So let's test our framework with the most common addback: the seller's salary. Say there is a husband-and-wife team, where the husband runs the day-to-day and pays himself $150K while the wife does bookkeeping at $75K. Both are retiring. What is an acceptable addback to cash flow? Let's run through our three questions.

Historically, these were recurring expenses. Post-close, you won't pay their salaries. But you will pay yourself and you will replace bookkeeping. If you'll pay yourself $125K and a third-party bookkeeping firm $25K, the addback is:

- Husband's Salary: $150,000

- Plus Wife's Salary: $75,000

- Less Buyer's Salary: $125,000

- Less Bookkeeping Firm: $25,000

- Total addback: $75,000, subject to test #3.

Can you prove it? Two common ways to validate owners' comp in SBA deals are (1) a line-item in the tax returns for "Compensation of Officers," or (2) a W-2 / 1099. If neither of those work, be ready with a strong explanation and documentation.

Other common addbacks (health insurance, personal vehicle expenses, retirement contributions, one-time broker prep fees) still need the framework. For example, if you add back the seller's health insurance, you should only add back the difference between the seller's cost and your post-close cost.

Harder claims include generalized "personal" travel and meals, one-time failed marketing campaigns, or costs tied to a fired employee "no longer needed." Once you run them through the framework, you see why they're problematic. Are they really non-recurring? You're never going to attempt to grow the business and perhaps strike out on some marketing expenses? And can you really verify that you don't need an employee's role anymore to generate the historical earnings? How do you prove these things?

A few other practical tips:

- Pro-forma rent adjustments. If the seller owns the real estate, rent may be below market. Confirm Day-1 rent. If the seller paid $2,000 per month and you'll pay $5,000, subtract $36,000 from annual cash flow.

- Evidence pre-LOI. In competitive deals, you may not get every document you want before going under LOI. Be clear on what you absolutely need versus what you can be flexible with learning post-LOI.

- Use a clear addback schedule. List each addback with the amount, a brief description, and the rationale defending the addback so it's easy for lenders to review.

- Consider a QofE. A QofE is not required to get SBA financing. However, if your deal is especially "addback heavy," a QofE will go a long way to giving you and your lender more confidence.

Tip #3: Position Yourself as the Perfect Buyer

Every lender's dream is a buyer who has spent twenty years doing exactly what the target company does in the same industry. But the reality is that most of the individuals we work with at BayCoast have no direct industry experience. That's OK.

What matters is whether you can make a strong, credible case that your background aligns with what the business actually needs on Day 1. Our best clients are passionate about how their experience lines up with the target. The stronger the story, the more attractive the deal. So how do you position yourself best to have that strong story?

Start by mapping the responsibilities of the owner you're replacing. What does the owner do every week? Who does he manage? What decisions land on his desk? Then define the business model. Is it a consumer marketing business at its core (with B2C lead gen, reviews, scheduling, and the like)? Is it a business with B2B sales and account management? A manufacturing business that lives or dies based on scheduling, quality control, and operations management? When you know the job, you can start to build a compelling case to lenders as to why you're the perfect person for it.

I can tell you this: simply understanding finance and deciding an industry is "hot" (looking at you, HVAC) doesn't make you the ideal person for it.

Here's a quick example from a former client. He left a corporate role in HR services and technology to buy a residential HVAC business. On paper, he had zero industry experience. He'd never turned a wrench. But in practice he was a perfect fit for this business. He was data-savvy, having worked on a variety of digital transformation initiatives over his career. He had built, grown, and managed large teams. He'd owned budgets and driven P&L results. And importantly, he'd grown up in a blue-collar family and worked residential construction, so he was ready to get in a crawl space.

Residential HVAC, at its core, is a consumer marketing business powered by a blue-collar workforce. He brought the digital transformation experience, operational experience, and leadership experience techs would follow. This made him an ideal buyer that lenders saw as a credible operator, despite never having worked in the HVAC industry before.

So here's what lenders want to see, and how you can show it:

- Map out the owner's responsibilities. Be able to say: "Here's what the seller does, and here's my experience that covers each item." If there are gaps, present a strong plan for how you're addressing those gaps.

- Demonstrate leadership and management experience. You don't need to have run a 100+ person org to get an SBA loan. But you do need real examples of leading people and owning outcomes.

- What's your angle? You should be able to describe the business and how it makes money, serves customers, and wins. What is it about your background that fits that business?

You don't need direct industry experience to position yourself as the perfect buyer. But if your sole positioning is "I'm smart, I'll figure it out," that isn't a great strategy.

Tip #4: Show the Cushion: Working Capital + Post-Closing Liquidity

Lenders don't just underwrite earnings, they also ask what happens if the business hits a slow month after closing. Do you have enough oxygen to breathe? Your job is to make sure you won't be so cash-strapped on day 1 that you're immediately at risk of missing a debt payment. Post-closing liquidity is the cushion that prevents a cash crunch.

Start with working capital. Pre-LOI, you may not get enough info from the broker to size up your working capital target (peg). If possible, get 12-24 months of balance sheets and calculate working capital the right way: current assets (A/R, inventory, WIP, and the like) minus current liabilities (A/P, accrued expenses, and the like), and exclude cash since most small-business acquisitions are cash-free, debt-free.

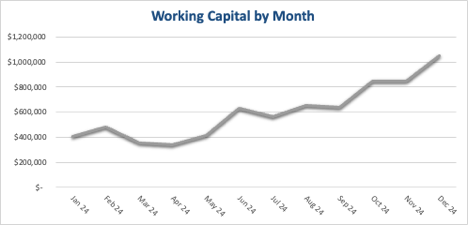

Next, plot working capital month-by-month so you can see the range and any seasonality. The chart below is a good example of why an "average" can get you in trouble. This was a B2B business that had several large enterprise customers, which would often lead to large A/R balances. Over this 12-month window, the average sits around $600K, but the year starts near $400K, dips in the spring, then stair-steps to north of $1.0M by year-end.

If you bought this business in May and funded it to about $400K, you'd be light when the Q4 A/R builds up. This is where working capital and post-closing liquidity can go hand-in-hand: when working capital swings are large, lenders want to see a real plan for dealing with those cash swings.

In other business models (like residential HVAC), you may even see negative working capital dynamics. In that case, working capital requirements are lower and post-closing liquidity is less important (on a relative basis). But you still need to plan for cushion to deal with inevitable issues that will come up post-closing.

Once you know your working capital requirements, you can start figuring out how much "cushion" you need in the form of excess cash to the balance sheet at closing, your personal liquidity, and any proposed lines of credit.

- Lines of credit. Work in an SBA Express line of credit at closing. You can size it up based on the business and the expected swings in cash flow, but it's important to get it done at closing. After closing, you may not be able to secure one.

- Excess cash to the balance sheet. Even if the seller is delivering working capital, you should consider extra Day 1 cash to cover the swings. Some lenders don't offer SBA Express lines of credit, in which case you should fund all your working capital needs and cushion right at closing as excess cash.

- Personal liquidity. Don't empty all your savings and liquid assets to make the down payment. Keep 3-6 months of personal expenses so you're able to sleep at night when your mortgage payment comes up.

How much is enough? Sometimes you'll hear rules of thumb thrown around, like 5-10% of the loan amount, or three months of fixed expenses, or even some minimum dollar amount. The right number will vary based on the lender and the business you are planning to acquire.

This is part of the value of working with an SBA financing advisor like BayCoast. We match you to lenders based on your specific deal and circumstances. If you think through these pieces up front, you're already showing up as the kind of buyer lenders want to lend to.

Tip #5: Address Key Risks in Your Deal Head-On

Every deal has risks. The strongest buyers don't shy away from them. They lean in, identify the top 3-5 risks, and present a strong plan to mitigate them, both in structure and in their business plan. Here is the best way to present them:

- Explain the risk in plain English, with specifics.

- Explain how you are mitigating the risk.

- Where possible, show the math (financial impact).

Here are two common examples of risks we've seen and some practical risk mitigation tactics buyers have used effectively.

Customer concentration. Who are the customers, and what % of revenue do they represent? Who owns the relationships? Provide a list with revenue by customer and a short narrative. For example, "The top 5 customers are about 50% of revenue. Historically, the seller was responsible for maintaining those relationships, but over the last 5 years the GM took over." To mitigate, describe the ways your deal structure is reducing the risk, along with any operational plans. For example, "I am working with the seller on a customer retention plan that involves direct introductions to customers, a renewal calendar, and a dedicated account manager post-closing. The seller is confident that these relationships will stay with the business and agreed to a contingent seller note. The note will be reduced or doesn't pay if top customers aren't retained." Then show the math: stress test what happens to revenue and earnings if you lose one or more of your top customers, and show the lender that you've thoughtfully considered the impact and structured the deal accordingly.

Key-man risk. Identify who the "indispensable" person is and what they do. Is it the seller, a GM, or a lead technician/estimator? Do they own customer relationships, pricing/bids, vendor terms, or technical know-how that no one else has? A clean way to present it is a role map with names next to responsibilities. For example: "Today, the seller handles enterprise sales, sets pricing, and approves major purchases; the GM runs scheduling and field ops." To mitigate, describe both the handoff plan and how you'll reduce single-point-of-failure risk. For example, "We have a 90-day transition plan with the seller that includes customer/vendor introductions, bid/estimating shadowing, and weekly knowledge-transfer meetings. The GM has signed a retention agreement with a milestone-based bonus. I'm taking sales ownership and have engaged an industry advisor who will help with complex bids. The seller has agreed to a non-compete/non-solicit and will be available on a consulting basis post-transition."

When you show both the structure and operating risk mitigants, and you've backed them with numbers, you're demonstrating you've thoughtfully considered the risks and protected yourself from the downside. That's the sort of thing that gets deals across the finish line.

Conclusion

Getting under LOI is hard. Closing is harder. If you (1) underwrite cash flow like a lender, (2) use only sensible, provable addbacks, (3) make a credible case that you are the right operator, (4) show real cushion in working capital and liquidity, and (5) outline the risks with clear mitigants and math, you'll stand out as a star to lenders. Do these five things well, and you won't just look like a buyer who can close, you'll look like an owner who can run the business on Day 1 and beyond.

Free pre-LOI consult. If you want a second set of eyes before you submit an LOI on a deal you're evaluating, book a free pre-LOI consult with BayCoast. We'll pressure-test structure, addbacks, DSCR, liquidity, and lender fit. Book a call or email me at drew@baycoastadvisors.com.